What was announced

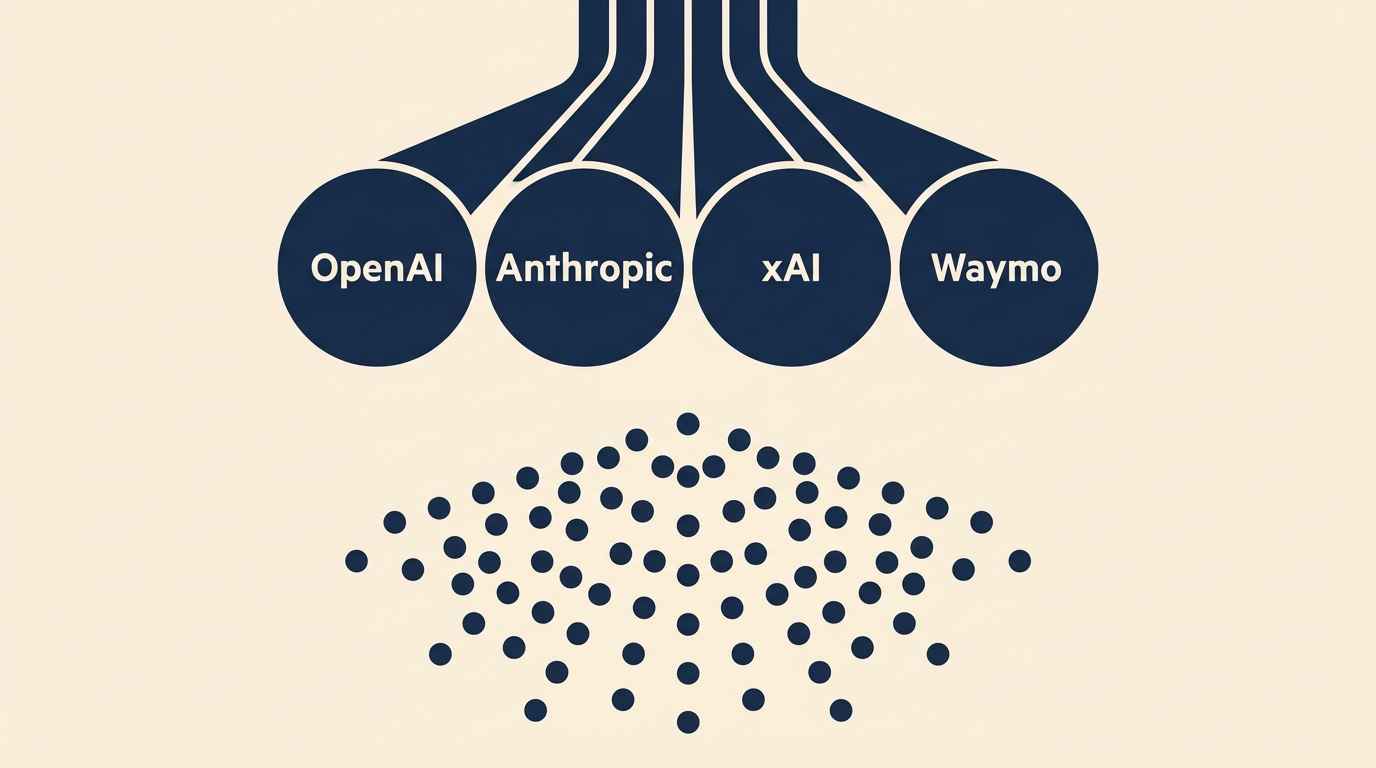

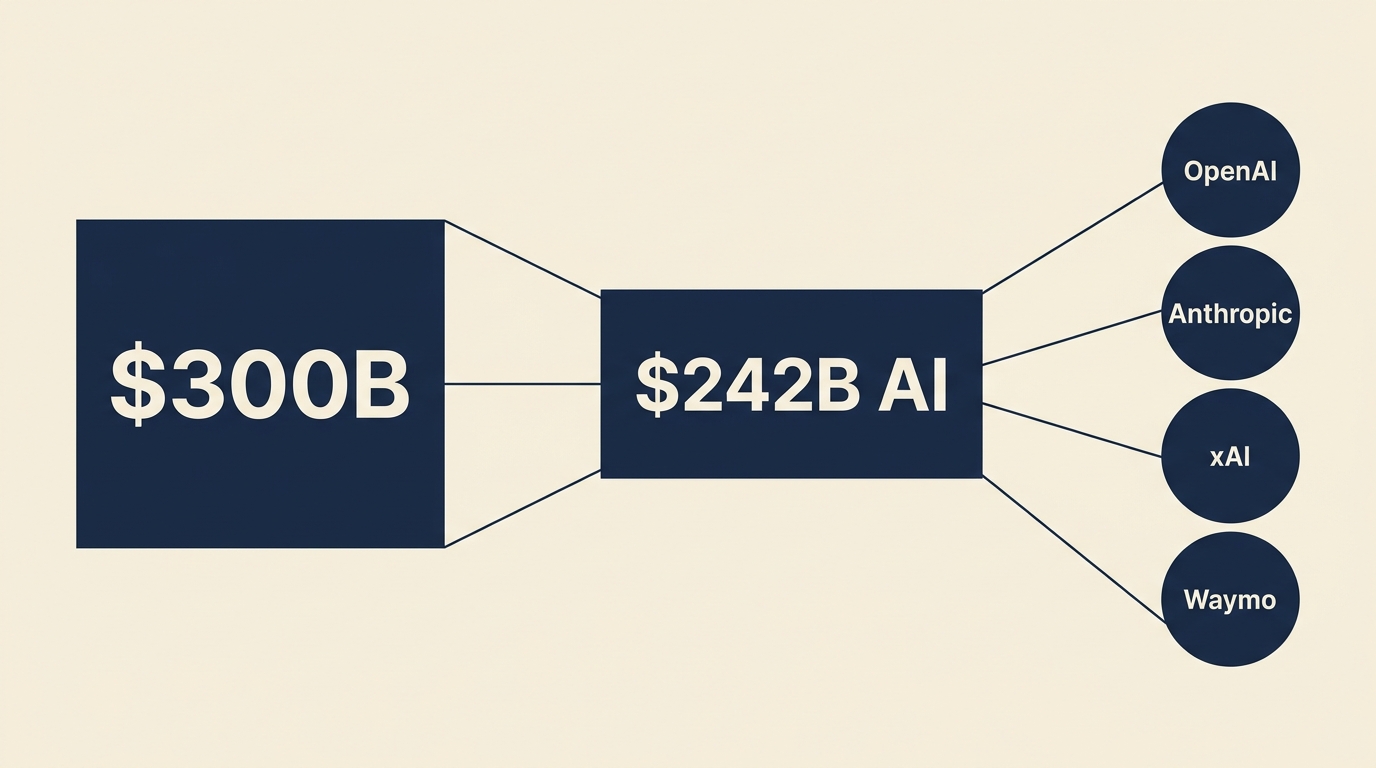

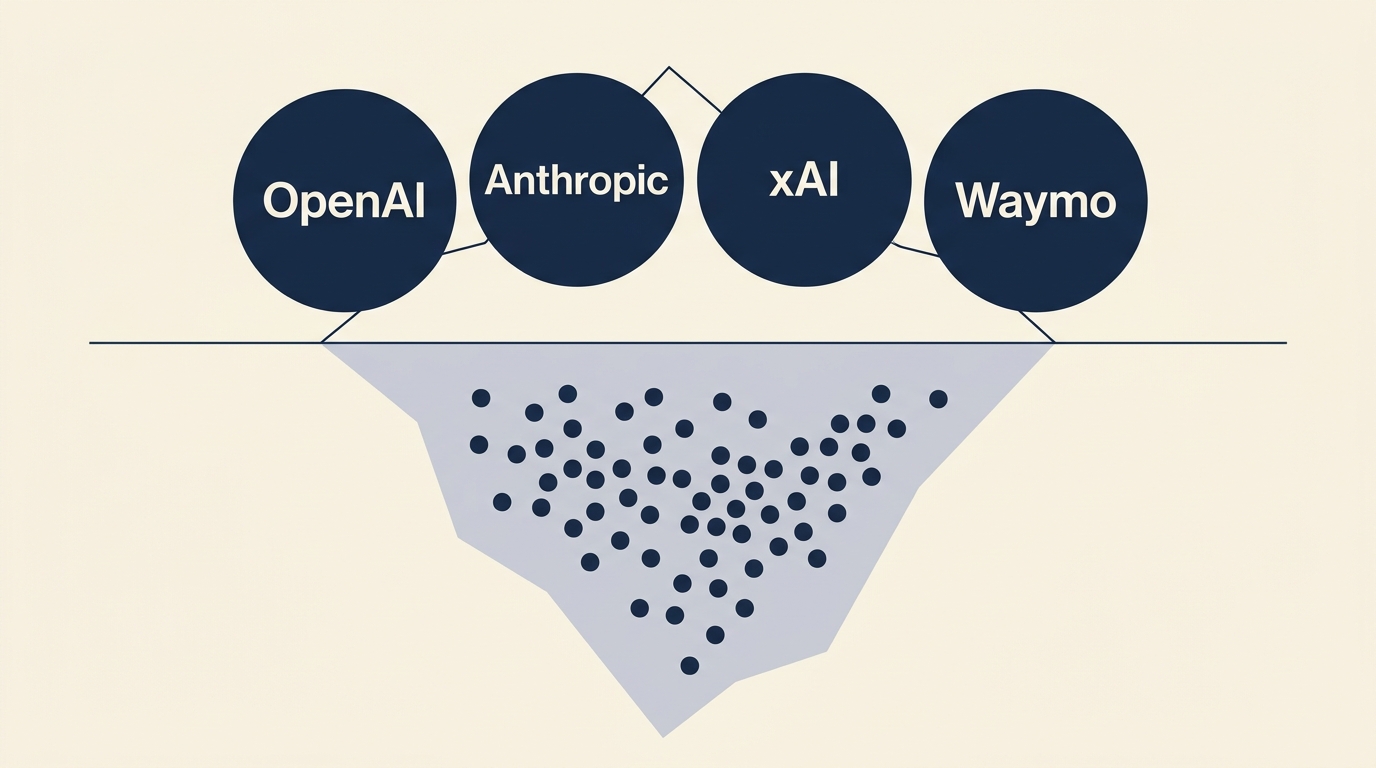

In Q1 2026, 47 startups crossed the billion-dollar valuation threshold for the first time — the largest single-quarter cohort in over three years. The pace is concentrated at the seed and early-stage end. Global venture funding hit roughly $300 billion in the quarter, of which 80% — about $242 billion — flowed to AI companies. Four companies (OpenAI, Anthropic, xAI, Waymo) absorbed 65% of all capital deployed.

What it means

Two things become visible at the same time. First, the market is willing to underwrite billion-dollar valuations earlier in the company lifecycle than at any point since the late-2020 boom. The valuation framework is no longer derived from realized revenue. It is derived from deployed compute and team density. Second, capital concentration at the top has reached a level where four companies define the cost of capital for everyone else. A new AI startup raising in 2026 is competing for the same dollars that just priced OpenAI at $122 billion.

The early-stage explosion and the late-stage concentration are two symptoms of the same conviction: capital has decided that AI is a winner-take-most market, and it is funding accordingly.

Andreas’s Take

My read on this: the unicorn count is a lagging indicator of a much earlier decision. That decision was made — quietly, by capital allocators — when the consensus shifted to a single conviction: AI capability gaps will widen, not narrow, over the next decade. From that conviction two strategies follow logically: fund the few names that might dominate the frontier (concentration), and over-fund the early stage so that whatever the next breakthrough looks like, you own a piece of it (proliferation). The 47 new unicorns are the proliferation half.

I don’t think this is a bubble in the conventional sense. A bubble is a price disconnect from fundamentals. What we’re seeing is a price connection to a forecast about fundamentals. If the forecast is right — capability gaps widen, AI returns accrue disproportionately to a few players — today’s valuations are conservative. If it’s wrong, half of these unicorns will not survive their next priced round.

What I’d say to boards and CFOs reading these numbers: don’t take comfort from “the market is hot.” Take instruction. Capital is signaling where it expects the next moat to form. The companies absorbing the capital are absorbing optionality, not just dollars.

Recommendation

Three things for leaders watching this market:

- Treat unicorn-count reports as competitive intelligence, not social proof. Look at which unicorns and what they are building — that is the signal of where the market expects gaps to open.

- Reassess your own compute and talent allocation against the new benchmark. If AI startups can attract billion-dollar valuations on team and compute alone, your incumbent organization is competing for the same talent at a different cost basis.

- Stress-test your strategic plan against a scenario where capability concentration plays out. What does your business look like if three or four frontier labs control the compute infrastructure and all serious AI deployment runs through them?

References and related signals

- Crunchbase: Q1 2026 venture funding shatters records — $300B global, 80% to AI

- TechCrunch (March 11, 2026): Almost 40 new unicorns minted YTD

- Crunchbase: January 2026 delivered the highest new unicorn count in more than three years

- Related Q1 mega-rounds: OpenAI $122B, Anthropic $30B, xAI $20B, Waymo $16B — four companies, 65% of global venture deployment

- Related infrastructure signal: hyperscaler 2026 capex commitments approaching $700 billion reinforce the same concentration thesis